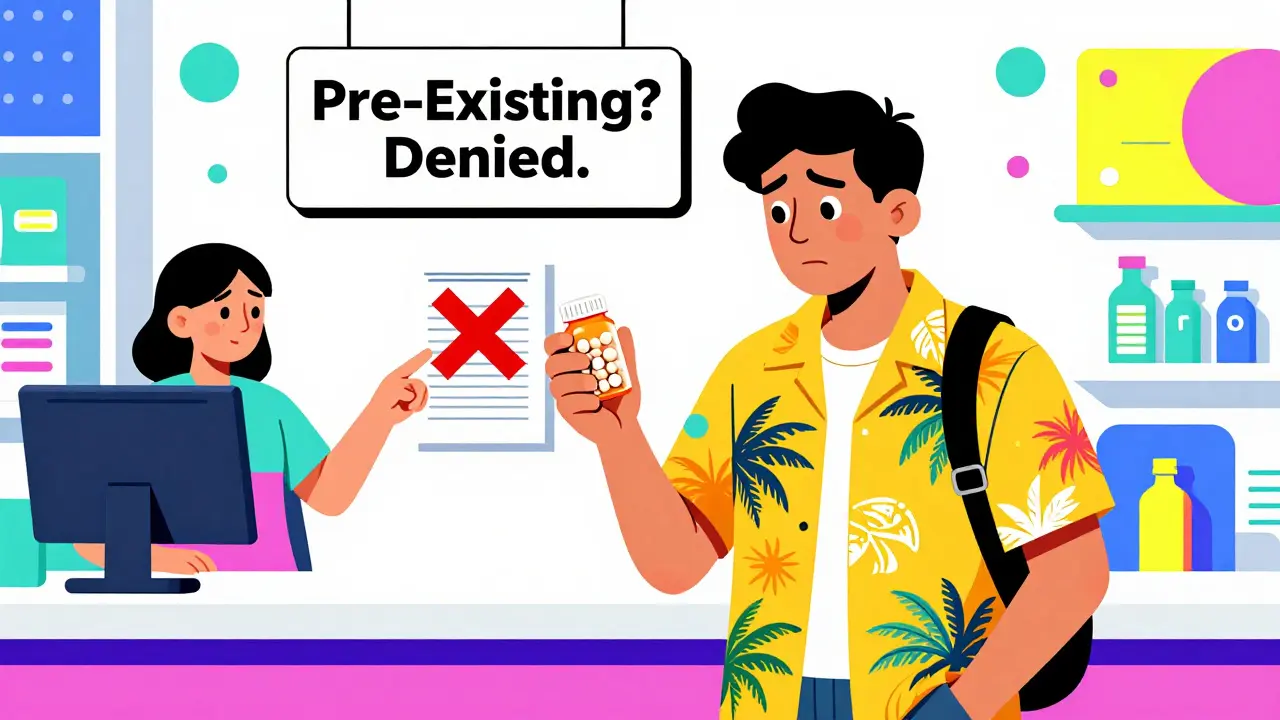

Imagine you're on a trip to Florida, and out of nowhere, you get sick. You need antibiotics. Or maybe you twist your ankle and the doctor prescribes painkillers. You head to the pharmacy, hand over your credit card, and the bill is $300. No problem, you think-you have travel insurance. But when you file a claim, it gets denied. Why? Because your insurance doesn't cover routine meds. Or because you didn't get a U.S. prescription. Or because you tried to refill your blood pressure pills after losing your bottle. These aren't rare stories. They happen every day.

What Travel Insurance Actually Covers for Medications

Most travel insurance policies don’t cover the meds you take every day. That’s not a loophole-it’s by design. If you’re on a daily prescription for high blood pressure, diabetes, or thyroid medication, your travel insurance won’t pay to refill it overseas. That’s considered maintenance, not an emergency. What they do cover are new, unexpected illnesses or injuries that happen while you’re traveling. For example, if you catch the flu and need an antibiotic, or you fall and need pain medication after a sprain, that’s covered. The policy kicks in only if the condition starts during your trip and wasn’t something you were already treating before you left home. Coverage limits vary, but typical plans offer between $5,000 and $250,000 for medication expenses over the entire trip. Some high-end plans, like Patriot Platinum or Seven Corners’ Trip Protection Choice, go even higher. Here’s how it usually works: you pay upfront at the pharmacy, then submit your receipts, prescription copy, and doctor’s note. Reimbursement takes about 7-14 days. Some insurers have direct billing with pharmacies like CVS or Walgreens, but that’s only if you use a network provider. If you go to a local pharmacy outside the network, you’re on your own until you file for reimbursement.The 90-Day Rule and Other Hidden Limits

One of the biggest surprises for travelers? Most policies cap how long a prescription can be filled-usually 90 days. That means if you’re traveling for six months and need a new prescription after three months, you’ll need to see a doctor again to get another one. You can’t just get a six-month supply and call it done. Another trap: you can’t use a foreign prescription in the U.S. Even if you brought your own pills from home and ran out, you can’t just walk into a U.S. pharmacy with a prescription from Australia, Canada, or Germany. U.S. law requires a doctor licensed in the U.S. to write the script. That’s why travelers who skip the doctor and try to refill meds on their own get denied. It’s not the insurance company being harsh-it’s federal regulation. And then there’s the deductible. Most plans have one, usually between $0 and $2,500. After you pay that, you might still owe 20% of the cost (called co-insurance). So if your meds cost $10,000, and your deductible is $250 with 80/20 co-insurance, you pay $250 + $1,500 (20% of the remaining $7,500) = $1,750 out of pocket. That’s still way better than paying the full $10,000, but it’s not free.What Travel Insurance Doesn’t Cover (And Why You’ll Get Denied)

The biggest reason claims get rejected? Misunderstanding what’s covered. Here’s what’s almost always excluded:- Pre-existing conditions-even if they’re stable. If you take insulin, your policy won’t cover a new prescription if you lose your bottle.

- Chronic disease meds: asthma inhalers, antidepressants, cholesterol pills, birth control.

- Over-the-counter drugs: ibuprofen, antihistamines, motion sickness pills-even if you need them for an acute flare-up.

- Medications bought outside the U.S. without a U.S. prescription.

- Refills of meds you brought from home that ran out.

How to Get Your Meds Covered-Step by Step

If you need medication while traveling, here’s how to make sure you get reimbursed:- Bring enough meds for your whole trip-plus a little extra. At least 10-15 days more than you think you’ll need. Store them in your carry-on, not checked luggage.

- Carry a copy of your prescription and a letter from your doctor explaining what the meds are for. Translate it if you’re going to a non-English-speaking country.

- If you get sick abroad, go to a doctor who can write a U.S.-style prescription. In the U.S., that means seeing a licensed physician. Telemedicine services from your insurer (like those offered by Allianz or IMG) can help you connect with a U.S. doctor remotely.

- Use network pharmacies if possible. CVS, Walgreens, and Rite Aid are common partners. Ask the pharmacist if they accept your insurance.

- Keep every receipt. It needs to show the medication name, dosage, price, date, and pharmacy name. Also keep the original prescription and any doctor’s notes.

- Submit claims fast. Most insurers require claims within 30-90 days of the expense. Use their app if they have one-it speeds things up.

Medicare, Credit Cards, and Other Myths

A lot of people assume Medicare covers them overseas. It doesn’t. Part B might pay for emergency care on a cruise ship within U.S. waters, but that’s it. Medicare Part D? Absolutely no coverage for drugs bought outside the U.S. Even if you have a Medigap plan (C, D, F, G, M, N), it only covers 80% of emergency care after a $250 deductible-with a lifetime cap of $50,000. And if you turned 65 after January 1, 2020, you can’t even get those plans anymore. What about credit card insurance? Most travel perks from Amex, Chase, or Visa are weak when it comes to meds. They usually cap coverage at $500-$1,000, have high deductibles, and often exclude prescriptions entirely. Don’t rely on them.Who Needs This the Most?

You might think young backpackers are the ones who need this. But the data says otherwise. Travelers over 55 make up 48% of all medication-related claims-even though they’re only 32% of international travelers. Why? Because they’re more likely to take multiple daily medications, have chronic conditions, and need prescriptions more often. If you’re in this group, or if you have a condition like diabetes, heart disease, or asthma, you’re at higher risk. A single missed dose can land you in the hospital. That’s why experts like Dr. Phyllis Kozarsky from the CDC’s Yellow Book say medical evacuation insurance is cheap compared to the cost of being stranded abroad. A medevac flight can cost $50,000 or more. Insurance that covers both meds and transport? Worth every dollar.

Top Providers and What They Offer

Not all travel insurance is created equal. Here’s how the big players stack up:| Provider | Max Medication Coverage | Deductible | Network Pharmacies | Telemedicine | Pre-Existing Condition Waiver? |

|---|---|---|---|---|---|

| IMG Global | $250,000 | $0-$2,500 | CVS, Walgreens, Rite Aid | Yes | Yes, with 14-day look-back |

| Seven Corners | $500,000 | $0-$2,500 | CVS, Walgreens | Yes | Yes, with 60-day stability period |

| Allianz Global Assistance | $100,000-$250,000 | $100-$2,500 | CVS, Walgreens | Yes | Yes, with 60-day stability |

| Patriot Platinum | $2,000,000 | $250 | CVS, Walgreens | Yes | Yes |

| Credit Card Insurance | $500-$1,000 | $100-$500 | No | No | No |

What’s Changing in 2025

The industry is evolving. More insurers now offer telemedicine consultations with U.S. doctors-82% as of early 2023. That means you can get a prescription without leaving your hotel room. Some are testing blockchain systems to verify prescriptions digitally, cutting down on paperwork and fraud. But the biggest change? Awareness. More travelers are learning that meds aren’t automatic. U.S. Travel Insurance Association predicts a 25% jump in medication coverage claims by 2025 as people become more informed. Still, only 18% of plans offer pre-existing condition waivers that cover related meds. That’s a huge gap. If you have a chronic illness, you need to shop for a plan that specifically includes this waiver-and you must buy it within 14-30 days of your initial trip deposit.Final Advice: Don’t Guess, Verify

Travel insurance isn’t just about flight delays or lost luggage. For people on meds, it’s about safety. A denied claim can mean going without your heart medication for days. That’s not a risk worth taking. Before you buy:- Read the fine print-not the marketing page.

- Call the insurer and ask: “Does this cover new prescriptions for acute conditions? What’s the max? What’s the deductible? Are network pharmacies listed?”

- Don’t assume your home insurance or credit card covers you.

- Bring extra meds. Always.

- If you need a refill, see a U.S. doctor first. No exceptions.

Does travel insurance cover my regular medications like blood pressure pills?

No. Travel insurance only covers new, unexpected illnesses or injuries that happen during your trip. Medications you take daily-like for high blood pressure, diabetes, or thyroid issues-are considered maintenance and are excluded. You must bring enough from home to last your entire trip, plus extra.

Can I get a prescription filled in the U.S. with a foreign prescription?

No. U.S. pharmacies are legally required to have a prescription written by a licensed U.S. doctor. Even if you have a valid prescription from Australia, Canada, or the UK, it won’t be honored. You must see a U.S. physician to get a new prescription.

How much does travel insurance cost for medication coverage?

It depends on your age, trip length, and coverage level. For a 30-day trip, basic plans start around $5 per day. Plans with higher limits (like $250,000) or pre-existing condition waivers cost $8-$12 per day. That’s far less than the cost of one emergency room visit or a single hospital stay.

What if I lose my medication while traveling?

If you lose your meds and they’re for a pre-existing condition, you’re out of luck-most policies won’t cover replacement. That’s why bringing extra is critical. If you develop a new illness after losing your meds, you can get coverage for that new condition, but not for the lost pills.

Do I need a doctor’s note to file a claim for medication?

Yes. To get reimbursed, you’ll need: an itemized pharmacy receipt, a copy of the U.S. prescription, and a doctor’s note linking the medication to a covered illness or injury. Without these, your claim will likely be denied.

Can I use telemedicine to get a prescription while abroad?

Yes. Most major providers like IMG, Seven Corners, and Allianz offer 24/7 telemedicine services. You can video-call a U.S.-licensed doctor who can write a prescription that’s valid at U.S. pharmacies. This is often the fastest and easiest way to get covered meds while traveling.

Is travel insurance worth it if I’m only going for a week?

Yes-if you’re going to a country with high medical costs like the U.S., Canada, or Western Europe. A single day in a U.S. hospital can cost $5,000. A prescription for antibiotics or pain meds can cost $200-$500. For $50-$100 total, travel insurance can protect you from thousands in unexpected bills.

February 1, 2026 AT 17:00 PM

bro i lost my insulin in thailand and thought my card would cover it... nope. had to call my dad to wire cash. never again. bring extra. always. 🤦♂️

February 3, 2026 AT 12:42 PM

It's not that the insurance companies are being malicious-it's that the entire U.S. healthcare infrastructure is built on the assumption that you're either insured domestically or you're not. The notion that you can just 'refill' a chronic condition abroad is a fantasy born of privilege and ignorance. You think your blood pressure meds are a human right? They're a liability to insurers. Deal with it.

February 4, 2026 AT 00:32 AM

I must emphasize: U.S. pharmacies are legally prohibited from honoring foreign prescriptions. This is not a policy choice-it is codified under the Federal Food, Drug, and Cosmetic Act, Section 505. Failure to obtain a U.S.-licensed prescription constitutes a violation of federal law, regardless of intent or circumstance.

February 5, 2026 AT 20:13 PM

i just want to say... if you're reading this and you're scared because you have meds you need daily? you're not alone. i've been there. bring extra. talk to your doc before you go. use telehealth. it's not perfect but it helps. you got this 💛

February 7, 2026 AT 17:33 PM

The fact that people still believe credit card insurance is sufficient reveals a systemic failure in public financial literacy. A $1,000 cap on medication coverage is laughable when a single day in a U.S. ER can cost ten times that. If you're traveling with chronic conditions, you're not 'traveling'-you're engaging in high-risk medical tourism. Plan accordingly, or don't complain when you're stranded.

February 8, 2026 AT 02:11 AM

real talk: i use img global. their app lets me video call a doc while sitting in a hostel in mexico. got my azithromycin script in 20 mins. paid $40, filed claim, got reimbursed in 9 days. the only thing better than the coverage? their customer service. no drama, just help.

February 9, 2026 AT 10:29 AM

It's interesting how we treat medication as both a personal necessity and a bureaucratic obstacle. We carry our pills like sacred relics, yet the system treats them as disposable liabilities. Perhaps the real issue isn't insurance-it's how we've outsourced health to institutions that profit from our vulnerability. What if we designed systems that saw people first, not risks?

February 9, 2026 AT 15:17 PM

I lost my pills in Barcelona and cried in a pharmacy because the guy didn't speak English. Then I used Allianz telemed. Doctor on Zoom. Prescription emailed to CVS. I picked it up 45 mins later. I didn't just survive-I thrived. If you're not using telemedicine on your next trip you're doing it wrong. #TravelSmart

February 9, 2026 AT 23:30 PM

so you brought 10 extra days of meds and still lost them? lol. maybe next time don't leave your bag unattended at the beach while you're dancing to reggaeton. also, i'm shocked anyone still uses credit card insurance. that's like bringing a toothpick to a knife fight.

February 10, 2026 AT 23:19 PM

I'm just here to say... if you're on meds and you think travel insurance is 'worth it'... you're already losing. 💀 The system doesn't care if you die. It just cares if you filed the form before midnight. #TravelInsuranceIsAScam